What's Happening in Austin Is Nothing Like 2008

Published | Posted by Dan Price

Understanding Austin’s Real Estate Drop in 2025

When people say "this isn't 2008," they're absolutely right—especially in Austin. The market dynamics we’re seeing today bear little resemblance to the housing collapse nearly two decades ago. Back then, Austin largely bypassed the national housing bubble. But this time, the city helped lead the surge—and is now experiencing a sharper correction.

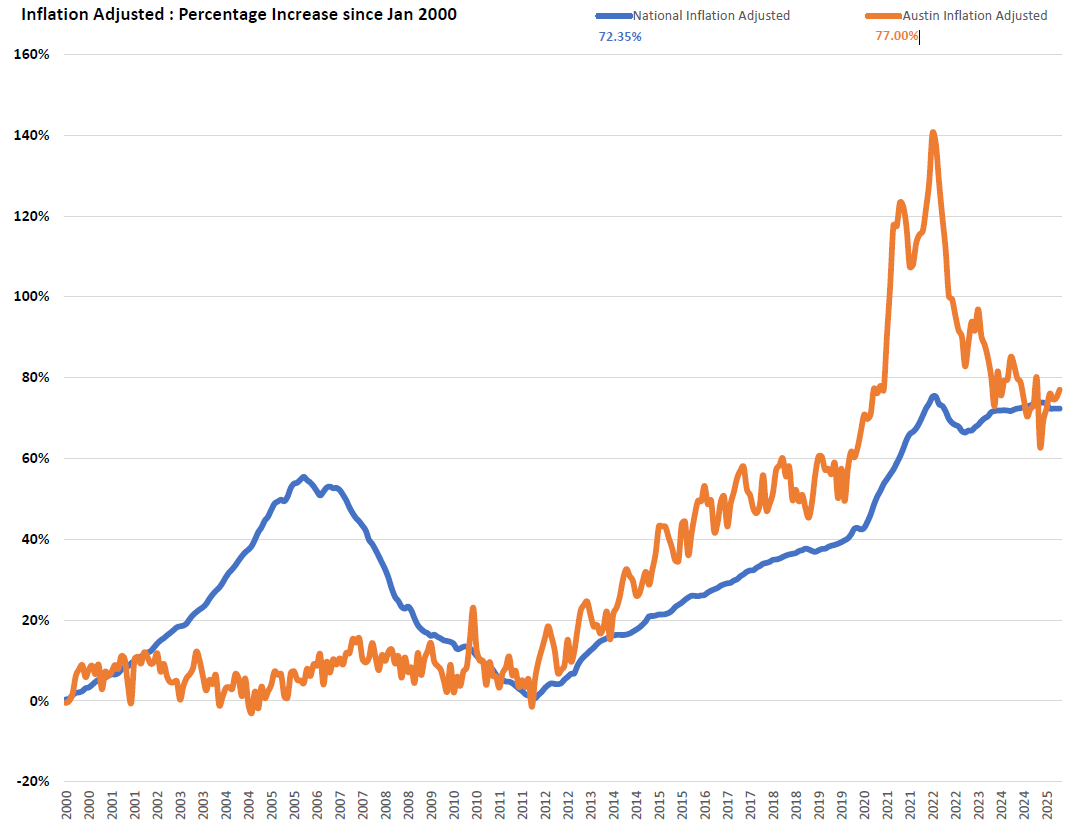

In 2008, Austin's housing market remained relatively stable. Nominal home prices (those not adjusted for inflation) didn’t experience a dramatic run-up in the years prior, so there was no major collapse when the national housing market unraveled. Unlike markets in California, Arizona, or Florida, where speculative buying and loose lending created unsustainable price spikes, Austin remained steady. Inflation-adjusted data confirms this: from 2000 through the early 2010s, Austin prices were flat or gradually rising in real terms.

But the 2020–2022 cycle was very different. Fueled by pandemic-driven migration, ultra-low interest rates, and investor demand, Austin home prices surged at record speed. By April 2022, Austin's inflation-adjusted home prices were up 140.5% from January 2000 levels. Nationally, inflation-adjusted home prices were up just 75.3% in the same period. Austin led the nation in appreciation.

Now, that momentum has reversed. In nominal terms, the median home price in Austin peaked at $550,000 in May 2022. As of July 2025, it's down to $450,000, a drop of $100,000, or -18.18%. That’s already a substantial correction. But the picture changes even more dramatically when you adjust for inflation.

Inflation reduces the value of each dollar over time. When we convert these nominal prices to inflation-adjusted dollars—measuring what today’s dollars are really worth compared to previous years—the decline becomes steeper. Austin’s peak real (inflation-adjusted) median price was $321,124 in April 2022. By July 2025, that number had dropped to $236,293, a decrease of $84,831, or -26.4%. That’s a much larger drop than the nominal figure suggests—and it matters for understanding how the market is truly performing.

Here’s why this distinction matters: nominal prices may appear stable or slightly down, but if inflation is high, your purchasing power is decreasing even as prices stay flat. In today’s high-inflation environment, a price of $450,000 in 2025 doesn’t buy what it did in 2022. That’s why economists and analysts adjust for inflation—to reflect the real value of money over time and to compare housing costs in an apples-to-apples way.

For example, if you bought a home in 2022 for $550,000 and today it's worth $450,000, you’ve lost $100,000 on paper. But in real, inflation-adjusted terms, you’ve lost closer to $85,000 in today’s purchasing power—and the overall impact feels more severe because the value of money itself has changed.

Back in 2008, Austin didn’t participate in the run-up, so it didn’t suffer the collapse. In 2022, Austin was at the center of the surge, and now it’s feeling the consequences of a rapid correction. This isn’t a foreclosure crisis or a financial system breakdown. It’s a price normalization, driven by a pullback from unsustainable highs.

What makes today different is not just the drop in prices—it's how quickly they rose before falling. The lesson? This is not 2008. But that doesn’t mean it isn’t painful.

FAQ

1. What’s the difference between nominal and inflation-adjusted home prices?

Nominal prices are the actual dollar amounts at the time of sale, without accounting for changes in the value of money. Inflation-adjusted prices reflect the real value of those dollars over time by accounting for inflation, giving a more accurate picture of long-term affordability and appreciation.

2. How much have Austin home prices dropped since their 2022 peak?

In nominal terms, Austin’s median home price has fallen from $550,000 in May 2022 to $450,000 in July 2025, an 18.18% drop. When adjusted for inflation, the decline is even steeper—down 26.4% in real purchasing power.

3. Why did Austin avoid the 2008 housing crash?

Austin didn’t experience the same pre-crash price spike that many other cities did. Without an extreme bubble in the early 2000s, the market had little to correct during the 2008 collapse. Prices remained relatively steady while other metros dropped sharply.

4. What caused Austin’s price surge in 2020–2022?

Historically low interest rates, remote work trends, a tech boom, and significant migration from higher-cost states all contributed to a spike in demand. This pushed Austin home prices up faster than almost any major city in the country.

5. Is Austin’s current price correction a crash?

No. The current correction reflects a reversal from unsustainable highs, not a systemic collapse. There’s no evidence of widespread foreclosures or financing issues. This is a valuation reset, not a repeat of 2008.

Related Articles

Keep reading other bits of knowledge from our team.

Request Info

Have a question about this article or want to learn more?